Business acquisitions continue to present strong lending opportunities, particularly as ownership transitions accelerate. While SBA 7(a) is often the primary financing tool, the SBA 504 program can be a powerful complement when an acquisition includes real estate or fixed equipment.

When structured properly, a 504 loan can improve borrower cash flow, enhance credit quality, and strengthen overall deal structure.

When the 504 Program fits

The 504 program is designed to finance owner-occupied commercial real estate and long-term fixed equipment, excluding rolling stock. When these assets are part of an acquisition, incorporating a 504 loan allows lenders to separate and optimize financing by asset class.

To qualify, the transaction must be structured as an asset sale, with the purchase price allocated across real estate, equipment, inventory, goodwill, and other components.

Valuation drives the structure

A key difference in 504 financing is that appraisals drive the loan structure. The portion allocated to real estate and eligible equipment must be supported by current third-party appraisals, which are required prior to SBA approval.

On a business acquisition, SBA cannot approve a 504 loan subject to appraisal – valuation must be established upfront.

What the 504 does not cover

The 504 program is limited to fixed assets and cannot finance:

- Inventory

- Rolling stock

- Working capital

- Goodwill

These components must be financed separately, typically through conventional lending, SBA 7(a) loans, or seller financing.

For transactions with significant goodwill, lenders should evaluate equity availability, potential seller notes, or the use of an SBA 7(a) loan to complete the capital stack.

Advantage of a 504 / 7(a) combo

Many acquisition structures benefit from a blended approach. The 504 program provides long-term, fixed-rate financing for real estate, while the 7(a) program addresses equipment – including rolling stock vehicles – as well as inventory and goodwill.

This combination allows lenders to deliver a more flexible and complete financing solution tailored to the assets being acquired.

Equity and credit considerations

Borrower equity requirements depend on management experience:

- Experienced buyers with relevant industry management or ownership experience for an existing business: Minimum 10% borrower contribution

- Less experienced buyers (new business): Minimum 15% borrower contribution

If the real estate is considered special purpose, SBA requires an additional 5% borrower contribution. Early structuring is critical to ensure these requirements are addressed upfront.

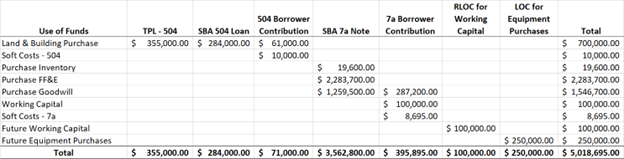

Case Study: Blended SBA Structure

A borrower with 20 years of experience acquired a full-service equipment rental company for $4.55 million, including real estate, equipment, inventory and goodwill.

- 504 loan financed the real estate;

- SBA 7(a) loan financed equipment, including rolling stock, as well as inventory and goodwill;

- Lender provided working capital and equipment lines.

This structure aligned financing with asset types while preserving liquidity for operations and growth.

504 Structure:

Overall Financing Structure:

Partnering early to maximize efficiency

The success of a 504-enhanced business acquisition hinges on early involvement and proactive structuring. Once a borrower has a Letter of Intent, engaging your WBD loan officer can help determine whether a 504 structure – or a combined 504 and 7(a) solution – is feasible.

WBD’s team works alongside lenders to navigate SBA requirements, evaluate eligibility, and develop structures that align with both credit objectives and borrower needs. Through our SBA 7(a) Lender Services, we can also assist in packaging companion 7(a) loans, simplifying execution and ensuring a cohesive financing approach.

Key takeaway for lenders

When a business acquisition includes owner-occupied real estate or long-term equipment, the SBA 504 program can be a powerful tool to:

- Improve borrower cash flow through fixed-rate financing;

- Strengthen overall deal structure;

- Reduce risk exposure through SBA participation;

- Expand financing flexibility when paired with SBA 7(a).

If you have a borrower under LOI to acquire a business, connect with your WBD loan officer early in the process to evaluate whether a 504 loan structure can enhance your next deal.